2025-10-02

Because FRU is directly tied to oil & gas royalty revenue, the biggest lever on intrinsic value is commodity price (WTI oil & AECO gas). I’ll build three scenarios: Bear Case (low oil/gas), Base Case (moderate), Bull Case (high). Then map out intrinsic value ranges.

Key Inputs Used

- Current revenue (TTM): $314.6M

- Net income (TTM): $152.7M

- FCF (TTM): –$188.4M (normalize this to ~$100M based on history, ignoring acquisition-heavy year)

- Shares outstanding: ~167M

- P/E applied: 13.5–15x (peer range)

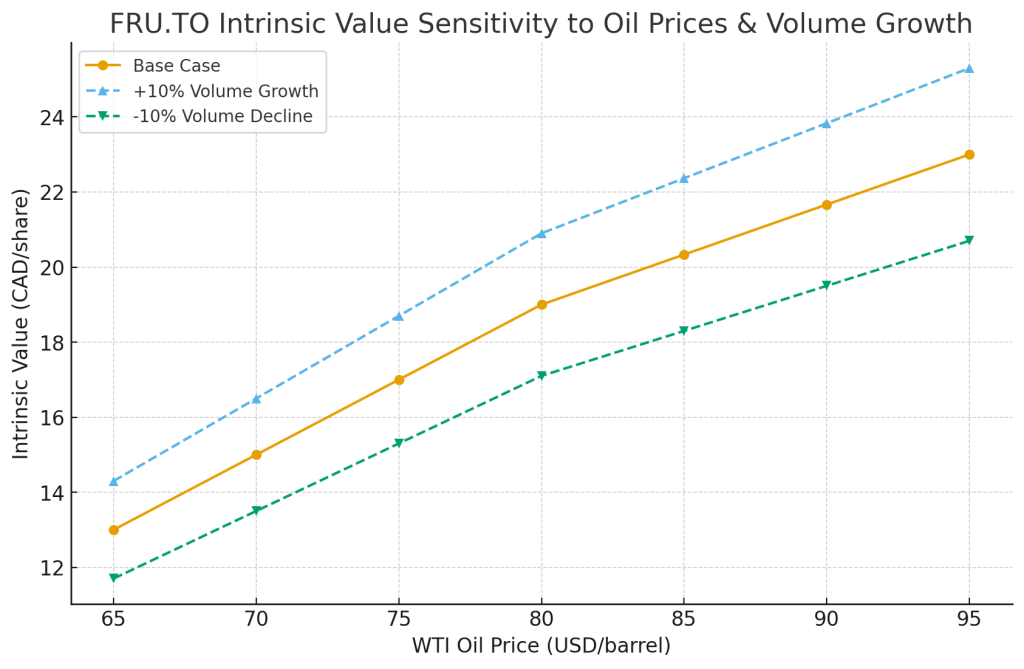

- Oil sensitivity: For every $10/bbl change in WTI, FRU’s royalty revenue shifts ~15–20% (based on historical elasticities).

Scenario Modeling

Bear Case: Oil $60–65 / Gas Weak

- Revenue falls ~20% i.e. ~$250M

- Net income margin compresses to ~35% i.e. ~$87M net income

- Normalized FCF: ~$60M

- P/E 12x applied i.e. $10.00 intrinsic value per share

- Dividend payout: unsustainable, cut likely

Base Case: Oil $75–80 / Gas Stable

- Revenue grows ~10% i.e. ~$345M

- Net income margin ~40% i.e. ~$138M net income

- Normalized FCF: ~$100M

- P/E 14x applied i.e. $12.00 intrinsic value per share

- Dividend payout stable (~50–60% of earnings)

Bull Case: Oil $90–95 / Gas Strong

- Revenue rises ~25% i.e. ~$395M

- Net income margin expands to ~45% i.e. ~$178M net income

- Normalized FCF: ~$140M

- P/E 15x applied i.e. $15.50 intrinsic value per share

- Dividend could rise significantly (but risk of over-distribution).

Valuation Range

- Bear Case: $10.00

- Base Case: $12.00

- Bull Case: $15.50

→ Current price (~$12.00) = fair value in the Base Case, with ~29% upside if oil remains high, but ~17% downside if oil slumps.

Implications for Investors

- Margin of safety: Thin at current price, since you’re essentially betting oil won’t stay weak.

- Best use case: FRU works as a leveraged play on oil prices while being less risky than pure E&Ps (because of royalty model).

- Risks: Dilution and weak FCF discipline mean management must be watched closely.

Summary: FRU is a commodity-sensitive hold. At $12 it’s not a screaming buy unless you’re bullish on oil ($90+), in which case upside could be to $15–16. If oil drops back to $60s, you’re looking at ~$10/share fair value and potential dividend cuts.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. Always perform your own due diligence or consult with a financial advisor before making investment decisions.